Deposit rates in Cyprus in 2026 remain significantly below the European average. New data from the European Central Bank show that Cypriot depositors continue to receive minimal returns on bank deposits, despite changes in monetary policy across the eurozone and the gradual recovery of the financial market.

The gap between Cyprus and Europe’s largest economies remains especially noticeable, with banks in those countries offering clients more favorable deposit terms. Experts link this situation to the high liquidity of Cypriot banks and limited competition within the local financial sector.

Deposit Rates for Businesses in Cyprus Have Risen Slightly

According to the latest ECB statistics, interest rates on fixed-term deposits for Cypriot companies rose to 1.35% in March 2026. For comparison, the figure was 1.13% a month earlier and 1.02% in March of last year.

Despite this increase, Cyprus remains among the eurozone countries with the lowest rates for corporate clients. Lower figures were recorded only in Bulgaria. At the same time, businesses in France and Slovenia receive more than 2% annually on similar deposit products. Financial analysts note that Cypriot banks do not face a liquidity shortage, so they are not interested in actively attracting additional funds by raising rates. This significantly limits companies’ ability to earn higher returns on their available capital.

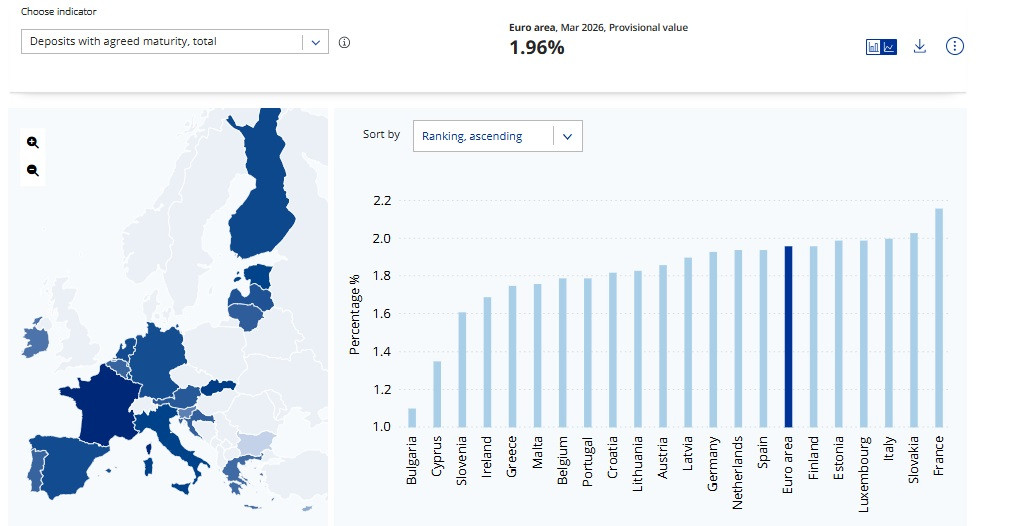

Individual Depositors Continue to Receive Minimal Interest

For private clients, the situation has remained virtually unchanged. The average rate on fixed-term deposits of up to one year in Cypriot banks stood at 1.18%, slightly below the February level. By this measure, Cyprus is among the weakest performers in the eurozone. Lower rates were recorded only in Slovenia, Greece, and Bulgaria. Meanwhile, banks in the Netherlands, Finland, and Italy offer depositors more than 2.3% annually.

The eurozone average currently stands at 1.82%, noticeably higher than the Cypriot level. Economists believe the gap between Cyprus and the rest of Europe may persist in the coming months, especially if the ECB continues its cautious reduction of key rates.

Why Cypriot Banks Are Not Rushing to Raise Deposit Returns

The Central Bank of Cyprus has repeatedly explained the weak dynamics of deposit rates by the excess liquidity in the banking system. After several years of strong inflows, the country’s financial institutions hold substantial reserves and do not need to attract new deposits aggressively.

Another factor is the small scale of the island’s banking market. The limited number of major players reduces competition, meaning banks face little serious pressure from clients. Experts also point to the low level of so-called pass-through — the speed at which ECB interest rate decisions are reflected in actual banking products. In Cyprus, this mechanism works significantly more slowly than in most eurozone countries.

What Is Happening with Loan Rates in 2026

Against the backdrop of weak deposit returns, Cyprus’s lending market is showing more positive dynamics. Interest rates on mortgage and business loans are gradually declining after the sharp increases seen in 2023–2024. This is linked to the gradual easing of European Central Bank policy and slowing inflation in the eurozone. As a result, loans in Cyprus are already cheaper than the European market average. Banking analysts expect competition for high-quality borrowers to intensify in the second half of 2026, especially in the mortgage lending and small business financing segments. However, a sharp rise in deposit rates is not expected for now.

Due to low deposit returns, many Cyprus residents are beginning to look for alternative ways to preserve and grow their capital. Increased interest is being seen in investment property, government bonds, investment funds, and international financial products. Continued inflation, which in some cases exceeds bank deposit returns, is creating an additional incentive to seek alternatives. As a result, real returns on deposits remain close to zero or even negative.

Financial consultants recommend that depositors closely monitor changes in ECB policy and compare offers from different banks, as conditions in the deposit market may change fairly quickly in an unstable economic environment.