The financial situation for depositors and borrowers in Cyprus has changed noticeably. Banks, seeking to preserve their interest margin, have become more active in increasing deposit yields while simultaneously shifting part of the costs onto loan clients through higher lending rates. According to the Central Bank of Cyprus, in December 2025 compared to November, an increase was recorded both in deposit rates and mortgage rates, indicating a change in the short-term trend in the market.

Such movement is occurring against the backdrop of a continued cautious monetary policy in the eurozone and market expectations regarding further decisions by the European Central Bank, which intensifies competition among banks for liquidity and stable sources of funding.

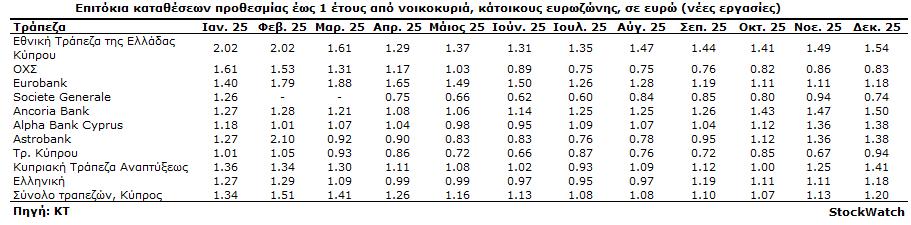

Deposits: yields continue to rise

The average rate on fixed-term deposits with a maturity of up to 1 year in December 2025 increased to 1.2% compared to 1.13% in November. Some banks strengthened their offers more noticeably than the market. National Bank of Greece in Cyprus raised the rate from 1.49% to 1.54%, and Eurobank Cyprus — from 1.11% to 1.18%. Ancoria Bank — from 1.47% to 1.5%, and Alpha Bank Cyprus — from 1.36% to 1.38%.

A particularly noticeable increase occurred at Bank of Cyprus, where the rate rose from 0.67% to 0.94%, while Cyprus Development Bank increased its figures from 1.25% to 1.41%. At the same time, not all market participants followed the path of increases. The Housing Finance Organization (HFC) slightly reduced its rate from 0.86% to 0.83%, and Societe Generale Cyprus recorded a decline from 0.94% to 0.74%.

Mortgages: growth after a pause

In the housing loan market, December 2025 saw a reversal of the previously downward trend. The average mortgage rate for home purchases increased to 3.11% from 2.96% in November, interrupting the period of decline. Eurobank raised the rate from 2.98% to 3.03%, while Bank of Cyprus showed a sharper increase from 2.98% to 3.25%.

At the same time, some banks reduced rates in an attempt to maintain competitiveness. Alpha Bank Cyprus lowered the indicator from 2.81% to 2.71%, Ancoria Bank — from 2.98% to 2.78%. A significant decrease was recorded at HFC, where the rate fell from 3.52% to 3.2%, and Cyprus Development Bank reduced it from 3.08% to 2.39%. Societe Generale Cyprus and the National Bank of Greece in Cyprus did not publish new data on mortgage rates for December.

What this means for the market and clients

December figures clearly show increased activity in banking strategies at year-end. Depositors received more attractive conditions for placing funds, while borrowers faced upward pressure on average mortgage rates despite targeted reductions by some banks. Against the background of ongoing inflation uncertainty and expectations regarding ECB rates in 2026, the Cyprus market will likely remain in a flexible adjustment mode, where deposits will be used as a key tool for attracting capital, and the cost of loans as a way to compensate for increased risks and expenses.