The Office of the Financial Ombudsman of Cyprus under the leadership of Valentini Georgiadou published new detailed statistics for 2025. The data reflect the number of complaints and mediation requests, as well as their outcomes. Particular interest is generated by cases that formally did not fall within the ombudsman’s jurisdiction but nevertheless led to the suspension or cancellation of 104 property repossession procedures, including primary residences.

437 requests outside jurisdiction and 104 homes saved

During 2025, the office received 437 requests. Of these, 215 concerned the suspension or cancellation of property repossession procedures, while another 222 related to other issues.

Despite formal limitations, in 107 cases it was possible to achieve the suspension or cancellation of 103 procedures involving primary residences and 4 involving second properties. In 89 cases, attempts to stop repossession were unsuccessful. In 19 cases, at the time of publication of the statistics, no response had been received from financial institutions.

These figures show that even outside the framework of direct powers, the intervention of the ombudsman can play a significant role in protecting homeowners in Cyprus, especially amid ongoing pressure on the real estate and lending markets.

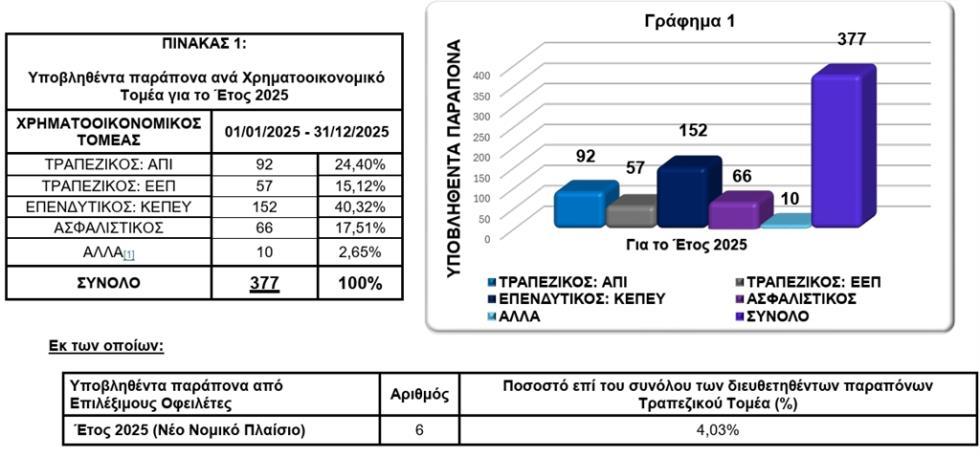

377 official complaints: banks, investment companies and insurers

During the entire year of 2025, 377 official complaints were submitted. Of these: 92 concerned banks, 57 — credit acquisition companies, 152 — Cypriot investment firms, 66 — insurance companies, and 10 — payment organizations and institutions related to electronic money.

Only 6 complaints, representing 4.03%, were submitted by so-called “eligible borrowers.” Recall that after legislative changes dated December 19, 2023, such borrowers received the right, after receiving notification, to file a complaint to verify the size of mortgage debt before the start of repossession procedures.

344 reviewed cases and decisions in favor of consumers

In 2025, the ombudsman’s office reviewed 344 complaints. Of these: 100 concerned banks, 58 — credit acquisition companies, 113 — investment firms, 64 — insurance companies, and 9 — payment institutions.

Of all resolved complaints, only 6 or 3.8% concerned eligible borrowers. In 58 cases, decisions were issued in favor of consumers; in 40 cases — in favor of financial institutions; and in another 15 cases, the parties reached a settlement agreement. Regarding the remaining 231 complaints, it was determined that they did not fall under the ombudsman’s jurisdiction, and their consideration was terminated.

Of the 58 decisions in favor of consumers, 20 were fully accepted by financial organizations, 10 — partially, 18 decisions were not accepted, and for 10 a response was pending at the time of publication. All companies that fully or partially agreed with the decisions fulfilled their conditions. In a number of cases, agreement was expressed as a gesture of goodwill without admission of liability.

According to current legislation, the parties have 2 months from the date of the decision to notify the ombudsman in writing about acceptance or rejection of the decision. If no response is received within this period, the decision is automatically considered rejected and loses binding force. Nevertheless, the office continues to accept responses even after this period to facilitate possible settlement.

Mediation: 20 applications and not a single successful appointment

In 2025, 20 applications were submitted for the appointment of a mediator. Of these, 5 were from bank clients and another 5 from clients of credit acquisition companies. A total of 12 such applications were reviewed during the year: 7 concerned banks and 5 concerned credit management companies. None of the 12 applications resulted in a successful mediator appointment. In 4 cases, the procedure ended unsuccessfully, 7 applications did not meet established requirements, and 1 was withdrawn by the applicant.

What this data means for the Cyprus market

The published statistics reflect a complex situation in the financial sector of Cyprus. On the one hand, a significant portion of applications remains outside the ombudsman’s jurisdiction. On the other — thanks to the intervention of the office, 104 property repossession procedures were stopped, which is especially important for the protection of primary residential property.

Against the backdrop of rising interest rates in previous years and gradual stabilization of the lending market in 2025, issues of mortgage debt and borrower protection remain at the center of public attention. The work of the financial ombudsman continues to play an important role in balancing the interests between banks and consumers.